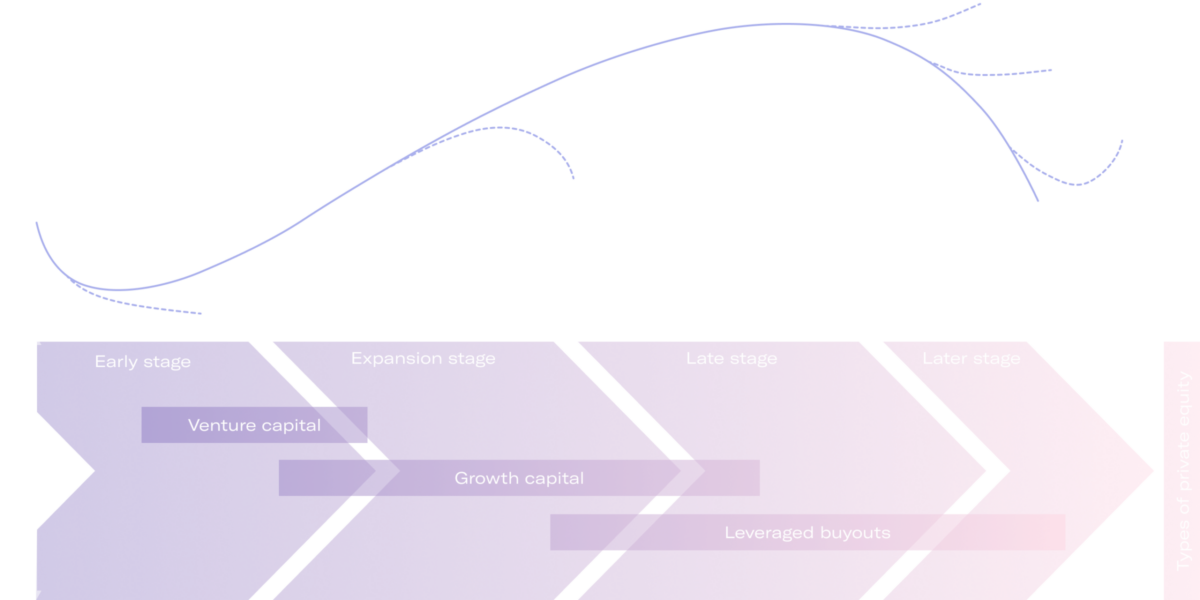

Type of private equity investment regarding the corporate lifecycle

Source: ResearchGate

The chart above also explains the low liquidity of private equity, seeing as such companies are not traded on public exchanges. This illiquidity is in fact the trade-off for the potential benefits of reduced exposure to general market fluctuations, as valuations are not subject to daily changes. It also makes these investments less volatile because investors can avoid panic selling due to the minimum holding period of approximately 10 years or more, and treat them as long-term oriented.

Another important benefit of private equity is access to emerging industries and technologies that are not easily accessible through public markets. Sectors such as artificial intelligence (AI), neurotechnology, and cleantech present substantial growth potential, yet only a few promising companies within these sectors have gone public and are available for investment by everyone.

The global AI market, for instance, is expected to reach around USD 2.57 trillion by 2032, growing at a compound annual growth rate (CAGR) of 19% from 2023 to 2032. Such significant market growth highlights the revolutionary role of AI. Given that the industry is relatively young, the reality is that most leading players are privately held. These companies have the greatest potential for growth and, consequently, investor returns, but sadly, those who don’t have access to these companies will miss out on most of the profit growth.

Last but not least is its low correlation with other asset classes, including public equities and bonds. According to Morningstar, private equity and the Morningstar US Market Index, which measures the performance of large-, mid-, and small-cap stocks in the US and represents the top 97% of the investible universe by market capitalization, have a correlation of 0.80, while venture capital and the same index have a correlation of 0.71. What’s more, the CFA Institute indicates that annual private equity IRRs and S&P 500 returns have a correlation of 0.15 over 25 years.

The superior performance of private markets and their low correlation with public market assets make them a great choice for portfolio diversification. A portfolio of low-to-negatively correlated assets can “dramatically reduce your risks without reducing your expected returns.” With enough portfolio diversification, investors are less likely to suffer major drawdowns, according to the “Holy Grail of Investing” Ray Dalio.

Making a handful of good uncorrelated bets that are balanced and leveraged well is the surest way of having a lot of upside without being exposed to unacceptable downside.

— Ray Dalio in his book Principles: Life and Work