In a recent primer on private equity secondaries, Moonshot explored the purposes, history, and performance record of the relatively new and, to most investors, little-known private equity secondaries market. That article could only scratch the surface, but a comprehensive analysis of this market’s current development, strengths, weaknesses, and prospects is essential for well-informed decision-making.

A Deep Dive into the World of Private Equity Secondaries

Aug 2024

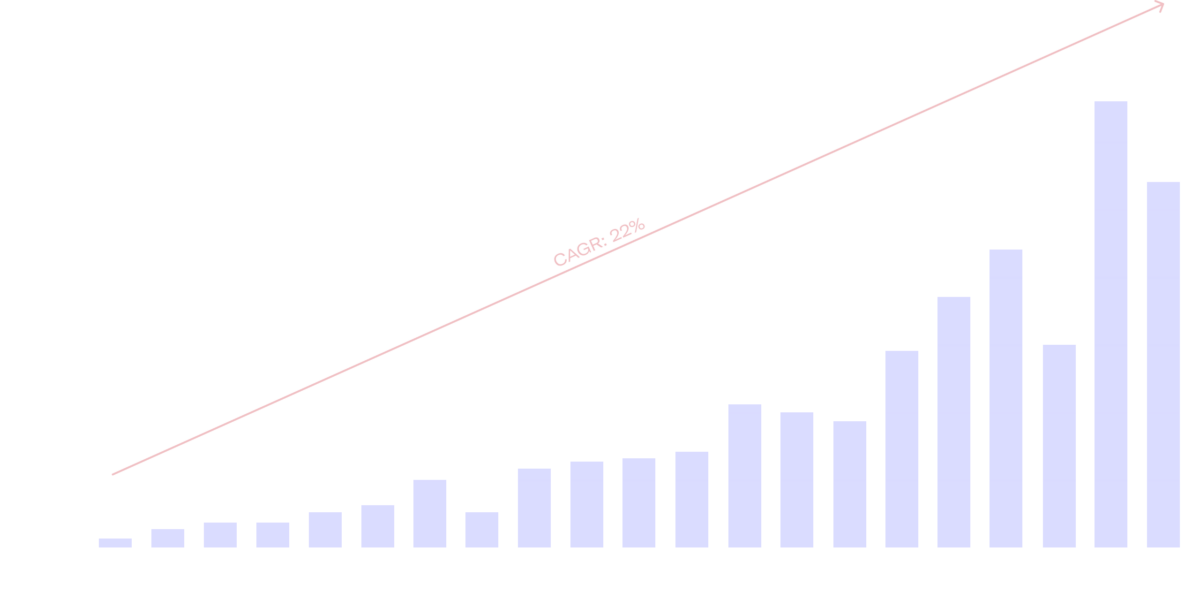

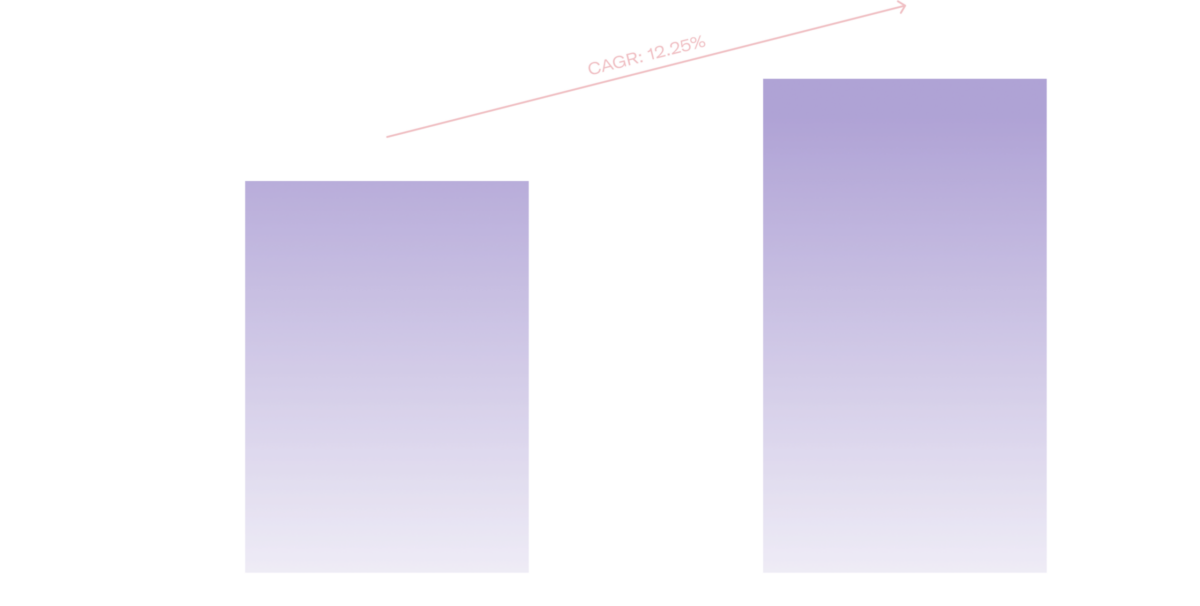

Worldwide secondaries deal volume and CAGR

Source: WTW

One of the key illustrations from our previous research suggests nearly 4 years have passed since the deal volume in secondaries attained its all-time annual peak: USD 132 billion in 2021. So what has been happening in the intervening years?

The Post-2021 Private Equity Secondaries Environment – What’s Changed?

As the chart shows, market activity fell significantly in 2022. The Russian invasion of Ukraine in February of that year helped drive a worldwide spike in inflation, to which the main OECD central banks, led by the US Federal Reserve, responded with their most aggressive series of interest rate increases in several decades.

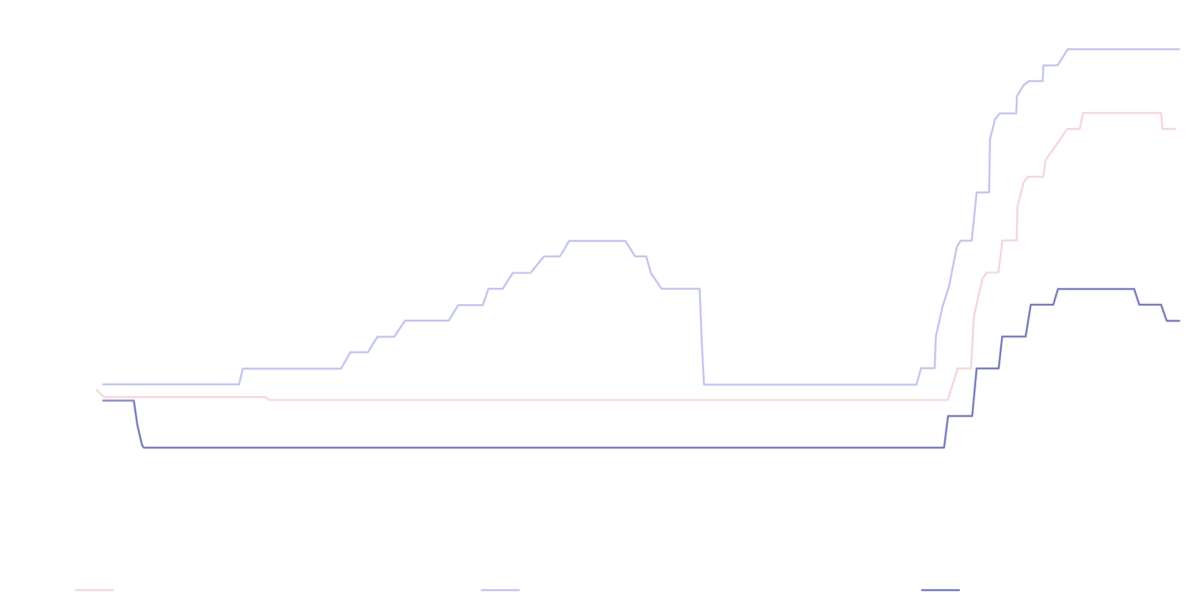

US (Federal Reserve), Switzerland (SNB), and Europe (ECB) interest rates since August 2014

Source: Trading Economics

Unsurprisingly, investor demand for risk assets of any type ebbed, not only PE secondaries. After enjoying a compound annual growth rate of 22% for 20 years, transactions fell by over 18% in 2022, to USD 108 billion. The total for 2023 has not yet been confirmed, but has been estimated at somewhere between USD 109 billion and USD 112 billion, perhaps indicating the low point has passed.

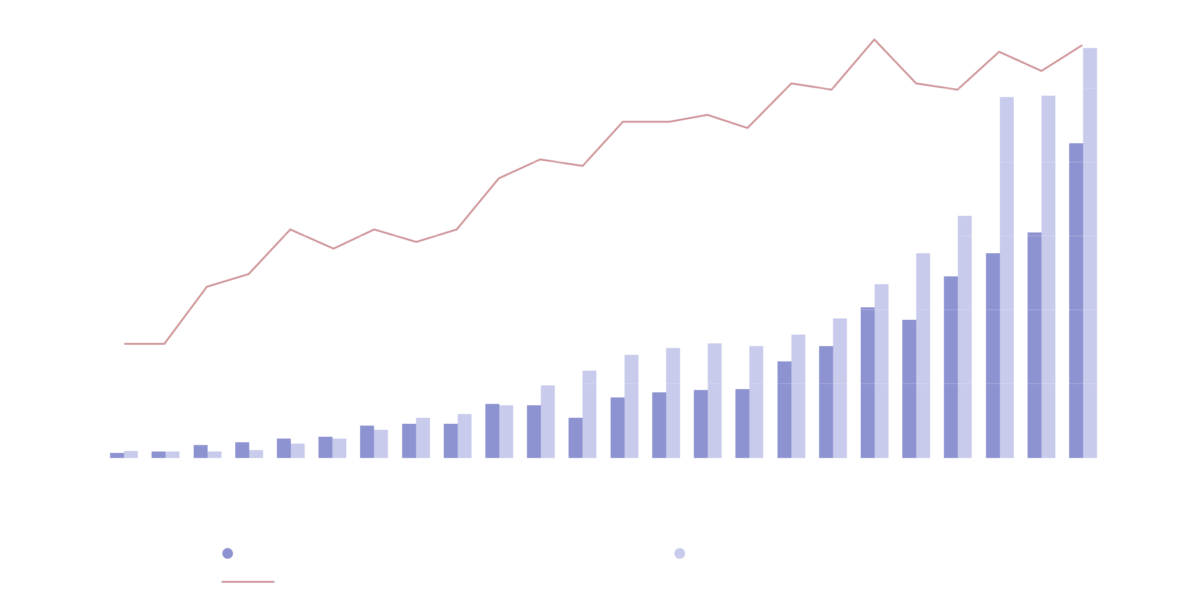

Underlying that optimism for the future is the growing demand for secondaries, indicated in the chart below by the strong growth in “dry powder.” Dry powder is the portion of the total assets raised by secondaries funds that remains uninvested and is represented by the blue sections of the columns in the chart below.

Private equity secondaries assets under management (AUM)

Source: Preqin

There is also further cause for optimism in that, despite transaction volume having grown more than 50 times in the past two decades, the total of assets under management in secondaries funds remains, by some estimates, at a modest eight percent of the total for all private equity funds.

Other analysts in this under-researched and opaque market claim the total is only about 1% of all private equity fund assets. Whatever the true figure, it is clear that the secondaries market remains a tiny part of private equity activities in general.

Meanwhile, the initiation of secondary transactions has changed significantly since the first secondaries fund was launched by VCFA in 1984. The biggest change has been in the size of the market and, even more, in the size of its participating funds. That first fund in 1984 raised just USD 6 million. Compare that with the world’s largest, the USD 22.2 billion raised in 2023 by PE mega-manager Blackstone for its latest secondaries fund.

Secondaries funds capital raised since 2013 (in USD billion)

Source: PitchBook

The Rise of GP-Led Transactions

The composition of the market has also transformed. It began with existing investors in PE funds, usually termed limited partners (LPs). Having been mainly the preserve of high-net-worth individuals (HNWIs) up to the 1980s, private equity funds became an important asset-class for institutional investors, especially American, and later European and Asian, pension schemes.

Unlike HNWIs, who invest their own money, institutional investors are fiduciaries to whom third parties entrust their assets for investment. Accordingly, they are governed by strict laws and regulations, especially respecting their risk management. When the success of their PE investments caused those positions to exceed their risk limits, the pension schemes were obliged to sell off part, or even all, of them to one or more secondaries funds.

Such over-allocation was exacerbated by the general setback in public markets after the 2022 invasion of Ukraine. Private markets were much less affected, thereby raising their weighting in diversified institutional portfolios even further and sharpening those asset-owners’ need to reduce their exposure.

Such “LP-led” transactions dominated the secondary market until quite recently. In 2021, however, secondaries initiated by general partners (GPs) ballooned. That was the result of waning investor appetite for initial public offerings. That development closed – partly, at least – the main exit route for the unlisted companies in which PE funds invest.

The market dominance of these “GP-led” secondaries has persisted and is expected to remain. The reasons are of both “push” and “pull” varieties. On the pull side, investor demand for secondaries is assured by the current level of dry powder. The record level of around USD 150 billion in 2022 has already been greatly exceeded in the first six months of this year, with an estimated total of no less than USD 189 billion outstanding. That is about 2.7 times the estimated USD 72 billion in secondary transactions turnover during the same period.

Private equity secondaries dry powder (in USD billion)

Source: Secondaries Investor, Preqin

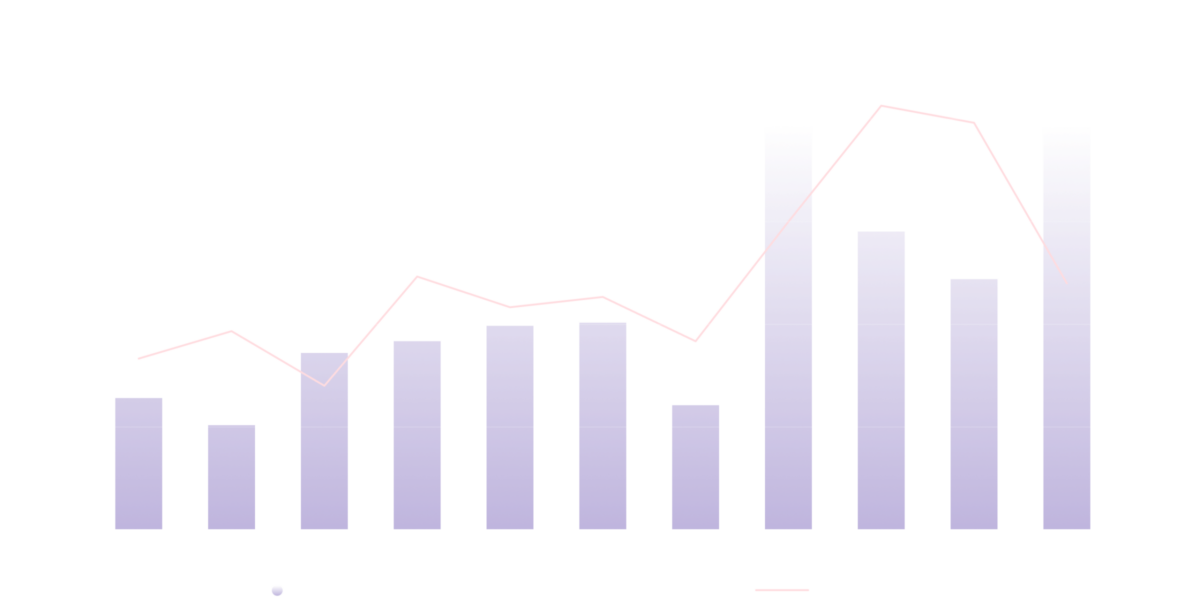

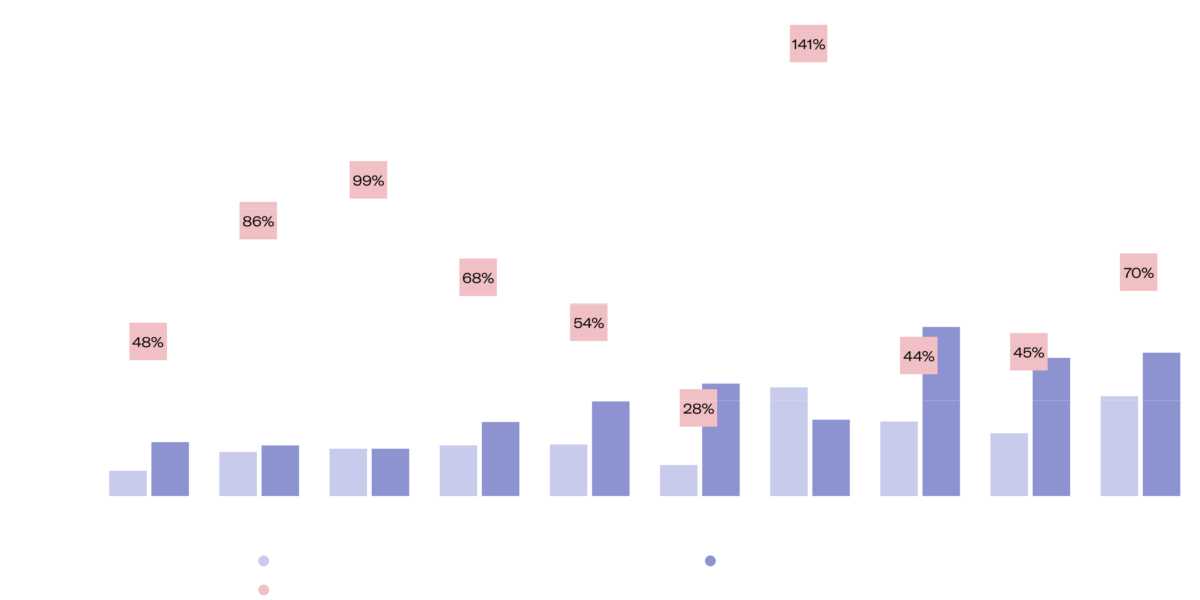

In terms of capital-raising, the entire secondary market seems to be running harder just to stay in the same place. That is because the sums raised by new fund launches, despite breaking records, are substantially outpaced by the rate at which those sums are being deployed in secondary deals.

New capital vs. new investment in the secondary market

Source: The Asset

As the chart above shows, transaction activity has been much greater than fundraising in each of the past ten years except for 2020. In fact, from 2021 to 2023, only 53 cents were raised for every dollar of new investment. The rest of the money came from sales of other investments, especially listed securities.

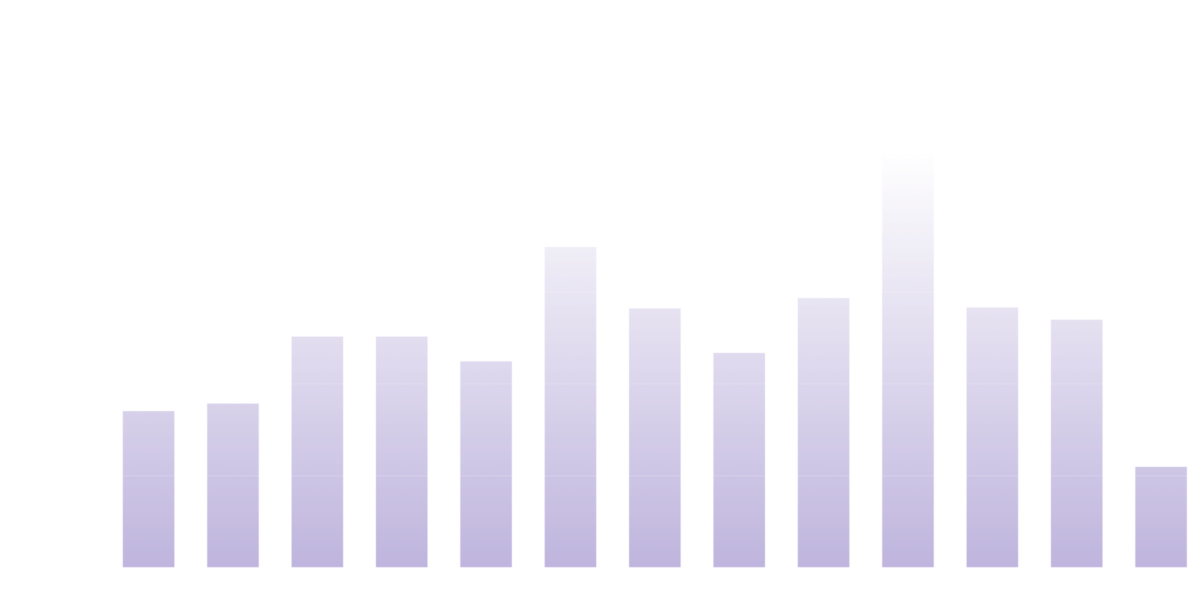

Market factors are also positive on the push, or supply, side. The main one can be found among buyout funds, which represent the dominant PE strategy (even greater than venture capital). Currently, those funds have some 28`'000 unsold positions in their portfolios, of which more than 40% have been held for four years or more. In terms of the value of those holdings, this is four times greater than was seen during the Global Financial Crisis (2007-09).

The significance of that holding period is that, typically, PE funds start “harvesting” (selling their portfolio positions) after four or five years. In short, PE fund managers are under pressure and need to start liquidating their portfolios pretty urgently. However, global IPO activity has been at historically average levels for almost three years. For want of a better alternative, therefore, GP-led transactions look as if they will continue to dominate the PE secondaries market for some time to come.

Global IPO activity by number of IPOs (from 2012 to H1 2024)

Source: Ernst & Young

Is This a Buyers’ Paradise?

For would-be investors, this could present a golden opportunity. Not only is there likely to be a plentiful and well-diversified supply of secondaries, but their pricing should be exceptionally attractive. However, this is a complicated market, with transactions conducted directly and in private between seller and buyer. Some look to trade entire portfolios, while others are only selling parts or just a single position – the latter are known as “mosaic” transactions. Pricing is, therefore, idiosyncratic.

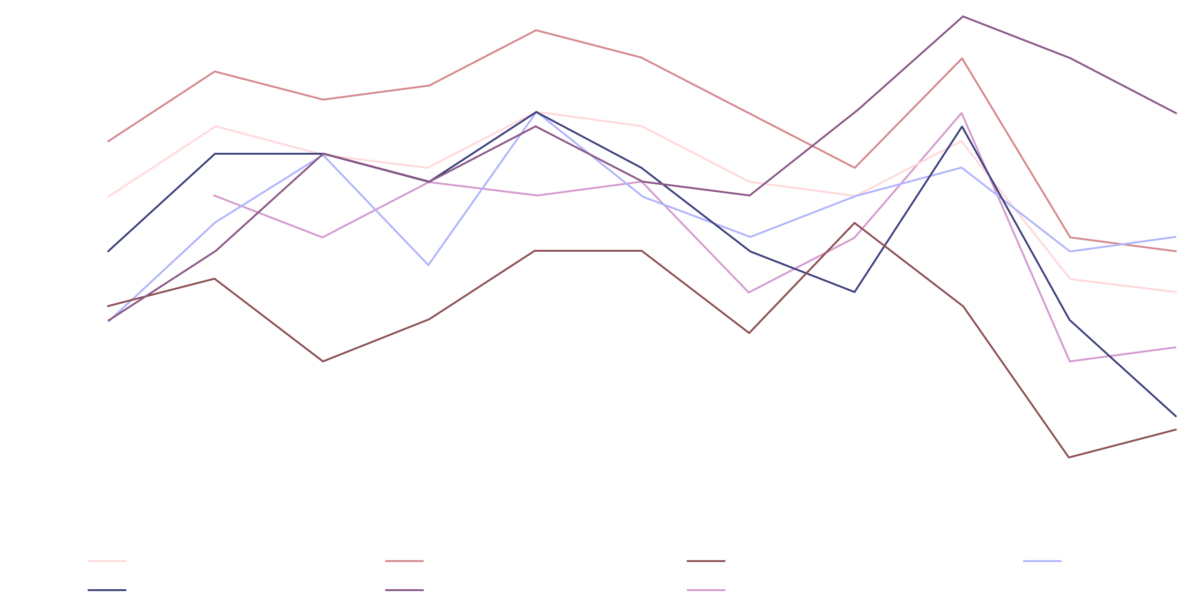

The chart below illustrates this point well. It records the trend of secondary transactions prices – expressed as a percentage of net asset value – over the past decade. Prices tumbled in 2021 and 2022 which seems perfectly logical given the dearth of IPOs at that time.

Private market assets historical secondary pricing as % of NAV

Source: Franklin Templeton

On the other hand, one may expect assets with lower risk to be traded at higher prices. Since 2022, that does seem to be the case, with infrastructure (which is seen as an income-producing asset with little risk) achieving the highest prices, and venture capital (VC) the lowest.

But why have recent sales of real estate funds been priced almost as cheaply as VC? Why was infrastructure so poorly valued ten years ago? Again, these anomalies reflect the opaque and multi-faceted nature of the PE secondary market, where each deal is unique. One buyer may want to acquire a varied portfolio of infrastructure funds, for example; another may want only a single discrete position in, say, toll bridges.

Above all, the prices reflect two crucial factors. The first is the maturity of the fund or investment being traded, with prices tending to rise for funds and investments that are nearer to their harvesting stage and which are, therefore, less risky. The second factor is closely related to the first. Private equity fund managers regularly look for more money from their investors to advance the business development of their individual investments.

The newer the investment is, the greater the future need for more capital. Any secondary buyer must assume responsibility for meeting such “capital calls” and that is reflected in a reduced price for the transaction.

Final Thoughts

From this analysis, it should be clear that PE secondaries are a complicated asset-class. The professional investors who are active in it employ teams of specialists to maintain myriad relationships with fund managers and intermediaries to source new opportunities, as well as to analyze and make investment recommendations.

None of that, however, is possible for the individual investor, though they still could invest in a secondaries fund. Those funds, however, are usually aimed exclusively at large investment institutions such as pension schemes, so they require minimum commitments that can be as much as several million, or even tens of millions, of francs.

Moonshot, in turn, enables individual investors to access these long-out-of-the-reach opportunities. We have a longstanding network of relationships with PE managers and intermediaries, as well as a team of dedicated experts to perform due diligence on the exclusive secondary opportunities we source through our network. As a Moonshot member, all you need to commit is USD 25’000 one-off – or, for some deals, USD 300 per month – in order to invest in the “best-of-breed” private equity opportunities offered on our platform.