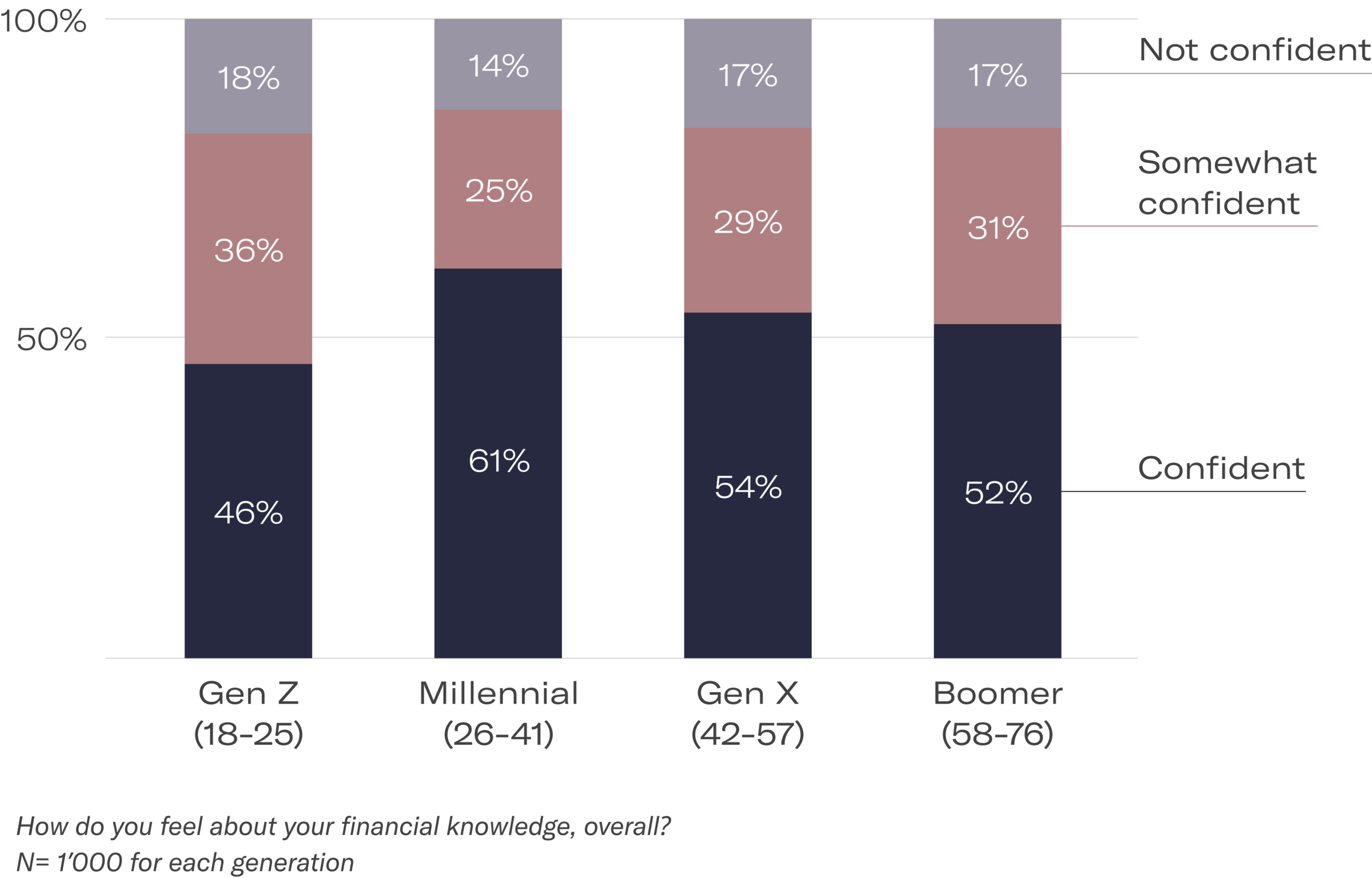

Mistakes young investors tend to make

We discussed how the margin of error can be much larger for young investors because the time horizon is longer. But just because there’s more leniency or opportunity for correction, doesn’t mean young investors should let their guard down. They can still make very costly missteps which can have severe consequences. We’ve outlined some of the most common mistakes young investors make below.

1. Taking financial advice from social media

This may seem paradoxical given the tech-savvy advantage young investors have. However, looking specifically at social media, there are countless self-proclaimed “experts” out there giving poor financial advice, whether it’s influencers on TikTok or anonymous commenters on obscure Reddit forums. For some of these uncredentialed “finance gurus,” their motivation is increasing their followers or engagement, rather than actually helping those who are consuming their content. It’s important to make sure you vet the content you consume and only seek out guidance from genuine advisors.

Vetting becomes quite the arduous task in addition to staying wary of popular trends, which are subject to groupthink and oftentimes are no more than a bandwagon for the next shiny new thing. The irony is that gold investing isn’t as popular as NFTs, yet what’s shinier than gold? Turns out, people are in fact looking to “combine” physical gold with NFTs to bring more inherent value to these tokens. Conventional wisdom may sometimes look dusty and boring in comparison to more exciting new developments, but there’s a reason certain strategies and investments have stood the test of time.

Gen Z should keep their guard up more than any other generation before them because they spend about 6.5 hours on their smartphone per day. But their screentime isn’t just for the sake of entertainment—many of them use social media or other apps as learning tools — how and when to start investing, and what all the terms and options mean.

A survey by Investopedia shows that Gen Z is the most video-forward generation in history, with YouTube being the most popular source at 45%, followed by conversations with friends and family (44%), internet searches (39%), TikTok (30%), and financial information websites (29%).

Most popular information sources by age group

Source: Investopedia

The same study shows that almost a quarter of Gen Z-ers are investing in crypto and stocks, and about 10 percent own NFTs.

Most popular investments by age group

Source: Investopedia

While technology can be a force for good and push the boundaries to pioneer new frontiers in the world of finance, there is a fine line between investing and simply speculating. Crypto investing and NFTs may fall into the latter category, as they are unproven in the long-term.

Everyone has that friend who swears by their crypto investments, but the reality is that the global crypto market has dropped below USD 1 trillion, having rapidly sunk from its peak of USD 3.2 trillion in the fall of 2021. Bitcoin, the largest and probably most well-known cryptocurrency, has itself fallen 70 percent during the same timeframe. That massive drop has wiped out years' worth of gains in mere months and is testing the faith of even the most fervent believers in digital assets.

All of this is not to say that more volatile (and flashier) types of investment like crypto investing or options are not legitimate — far from it. These new frontiers are necessary to push the boundaries of what’s possible. What Gen Z may lack in earning power from a salary compared to other generations, they could vastly make up for it with their bandwidth for risk tolerance, owing to their longer time horizons for investing.

But to achieve long-term stability and wealth, these types of high-risk investments need to be balanced with time-tested “safer” methodologies. Thus, while social media may be flecked with nuggets of wisdom, investors in their 20s (or any age, for that matter) should look at it with a critical eye.

2. Investing without due diligence

Opportunities that are too good to be true most likely are. It’s important to understand that every form of investing involves risk, so statements like “zero risk” or absurdly high guarantees as to future returns are red flags.

The most effective way to avoid being duped or making a poor investment decision is by doing your research. Not only is it essential to research the asset you are considering investing in, but you should make sure the platform you’re using is credible. Cross-referencing of reviews and features can help, but also a look out for subtle red flags that pop up in the language being used to market these products. Extremely high returns or inflated metrics may be a good indicator for suspicion. The best way to know what’s real and working and what isn’t is by taking the time to understand the platform or asset.

3. Underestimating diversification

A concept that rivals, if not surpasses, compounding in its importance is diversification. The idea is simple: Invest in a range of different ways to lower your risk. For instance, if the stock market is reeling in the wake of an economic downturn, bonds may remain relatively stable, so if you allocate your portfolio to 60% stocks and 40% private equity, you are exposed to a much lower level of risk than if you had allocated 100% of your portfolio to stocks.

That’s one example, but there are several ways to diversify, whether by investing in diverse markets, asset class, strategies, investment types, risk, etc. It goes back to the old adage of not putting all your eggs in one basket.

On average, well-diversified portfolios generate higher returns in the long-term. It’s a tried and tested methodology that any young investors should apply to their strategy, so don’t underestimate it.

4. Not investing at all

The worst mistake a young person can make is not investing at all. As mentioned above, young investors have the distinct advantage of time on their side. Time is an irretrievable resource. Rather than spending money casually now, seize the opportunity presented by long time horizons and compounding.

We can’t overstate the importance of investing early. Younger people tend to feel stretched thin financially with student loans, lower-paying jobs, and starting families. It can seem a difficult task to allocate a percentage of earnings to an investment portfolio, but making this into a consistent habit will send them on a path to future wealth, even if it requires a sacrifice in the present.

Now that we’ve looked at some of the benefits of investing young and mistakes to avoid, what types of investing should you consider?